Share options for permanent employees of the Festi hf. group

Permanent Employees Who Joined the Group After April 1, 2024

Permanent employees who joined the Group after April 1, 2024, and have not previously been offered to sign a share option agreement, are now being offered the opportunity to sign a share option agreement for a two-year period. This also applies to permanent employees of Lyfja and Heilsa who became part of the Group after April 1, 2024. Permanent employees are defined as employees with an indefinite employment contract with a company owned by Festi hf.

• The share option agreement grants the right to purchase shares in Festi in accordance with the terms of the agreement but does not entail an obligation to purchase.

• The share option agreement must be signed between April 30 and May 6, 2025.

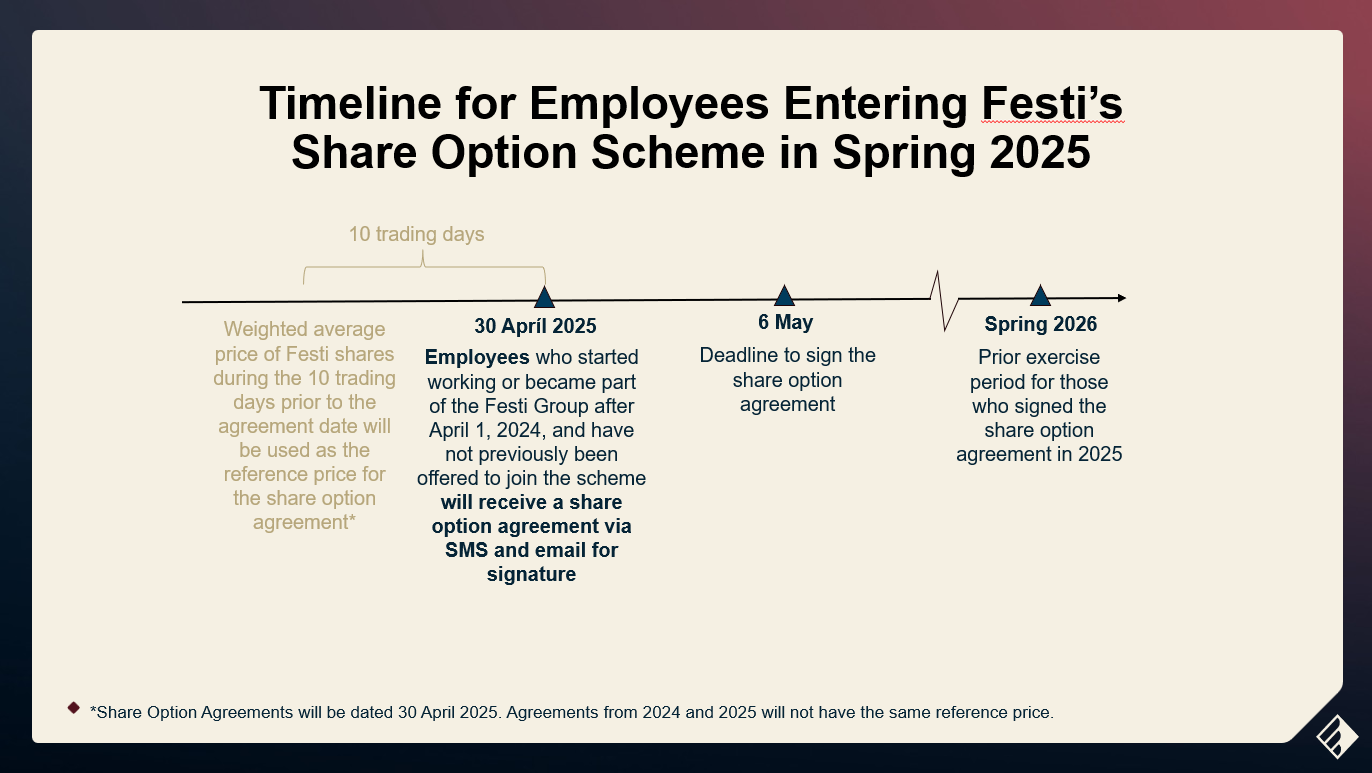

• The reference share price for the share option agreement will be calculated as the average price of Festi shares over the 10-day period preceding April 30, 2025.

• The exercise periods for the share options are two, starting from the signing of the share option agreement. The first exercise period will be in May 2026 and the second in May 2027.

✍️ How Do I Sign the Share Option Agreement?

• On April 30, 2025, Festi will send a share option agreement to everyone eligible to enter the share option scheme now.

• Employees who sign the share option agreement this year will be permitted to purchase shares in the company for up to ISK 500,000 during each exercise period, or for a total of ISK 1,000,000 over the entire share option period.

• To obtain share options, the share option agreement must be signed between April 30 and May 6, 2025.

• If you are under 18 years of age, your guardian will receive the share option agreement, which they must approve and sign on your behalf.

• If you do not sign now, you will not get another opportunity to join the scheme.

🤔 When Can I Exercise the Share Option if I Sign the Agreement This Year?

• The share option exercise period begins 12 months after signing the share option agreement, meaning you cannot exercise the option immediately.

• There are two exercise periods following the signing of the share option agreement.

• The first exercise period will be in May 2026 and the second in May 2027.

• After the second exercise period (May 2027), the right will expire.

🧾 Do I Need to Do Anything Now?

• No – further information about the share option agreements and next steps will be sent to employees.

Q&A – Share options for permanent employees

1. What is a share option?

A share option is an agreement that grants permanently employees of the Festi Group the right to buy shares in Festi for a certain amount or a certain number of shares, at a predetermined price, within a defined time frame. Under such a share option agreement, you will thus be granted the right to buy shares in Festi at the beginning of May over the next two years at a predetermined price. You will not become obligated to buy any shares if you sign the agreement; you will merely have the right to do so. If you decide not to exercise this option when it becomes available to you, it will simply expire at the end of the two-year period.

The option to buy shares under the agreement will first become exercisable at the beginning of May 2026.

Festi is a listed company on Nasdaq Iceland, and its shares are publicly traded. Share price information can be accessed at: https://keldan.is/Markadir/Hlutabref/FESTI

2. Why is Festi offering stock options to its employees?

The aim is to align the interests of employees with the performance and long-term goals of Festi and its shareholders. This creates a financial incentive for employees, as they are given the opportunity to participate in the increase in the value of Festi resulting from the good financial results that their work will create.

3. Do I automatically acquire the share option, or do I need to take action?

You do not automatically acquire a share option; instead, a written agreement must be made in each case between you and Festi regarding such an option.

All permanently employed staff who started after 1 April 2024, are invited to conclude a share option agreement with Festi before the end of 6 May 2025.

4. Am I obligated to enter into a share option agreement?

No, you are not obligated to enter into a share option agreement with Festi. You are only being invited to enter into a share option agreement and acquire the rights that come with it, but it is up to you whether to enter into a share option agreement or not.

If you decide not to enter into a share option agreement with Festi, you will not acquire an option to buy shares in the company.

5. Are share options available to all employees of the Group?

All permanently employed staff as of 31 March 2024, regardless of employment ratio, were eligible last year. This year, permanent employees who started after 1 April 2024, have the opportunity to join in the share option scheme.

Temporary or short-term employees are not eligible.

6. In what languages is information about the stock option available?

You can access general information about the share option scheme in Icelandic and English.

The share option agreement that you are invited to enter into will be in Icelandic.

7. How do I conclude a share option agreement?

Festi will invite you to conclude a share option agreement with the company. If you choose to enter into a share option agreement for shares in Festi, such an agreement will be sent to you on Wednesday 30 April 2025, in electronic form for review and signature through an electronic signature process. If you decide to accept the invitation to conclude a share option agreement, you must sign the share option agreement by the end of day on Tuesday 6 May 2025.

If you do not sign the share option agreement within the required time limit, the share option will be cancelled and you will no longer be able to participate in the share option scheme.

8. Do I need to pay a purchase price or make some other payment when I sign the share option agreement?

No, you do not need to pay anything when you sign the share option agreement. The share option agreement will provide for your right to purchase shares at a specified price during pre-defined exercise periods that will occur annually over the next two years. When it comes to exercise periods, you need to decide if and to what extent you wish to exercise your share option - and then, if you decide to exercise the option, pay for the purchased shares in accordance with the terms of the share option agreement.

Further details will be sent in April 2026 to those who sign the share option agreement by the end of day on Tuesday, May 6 2025.

9. I am under 18 years old – can I enter into the agreement?

Yes, you can enter into a share option agreement if you are a permanent employee of the Group. If you are under 18 years of age and intend to enter into a share option agreement, the agreement must also be approved by a parent or guardian on your behalf. The parent or guardian will be sent such an agreement on Wednesday, 30 April 2025 in electronic form for review and confirmation through an electronic signature process.

10. When can I exercise the stock option, and are there limits?

The stock option period is two years and divided as follows:

1) The first period is from the date of the share option agreement until one year has passed since that date (beginning of May 2026).

a) At the end of the first period, employees will have the option to buy shares in Festi for up to ISK 500,000.

b) Employees must issue an exercise notice within ten (10) business days from the publication of Festi's quarterly results for the 1st quarter of 2026 if they wish to exercise the share option.

c) Unexercised options will be carried over to the next exercise period.

2) The second period is from the end of the first period until one year has passed since that date (beginning of May 2027).

a) At the end of the second period, employees will have the option to buy shares in Festi for up to ISK 500,000.

b) Employees must issue an exercise notice within ten (10) business days from the publication of Festi's quarterly results for the 1st quarter of 2027 if they wish to exercise the share option.

c) Unexcercised options will expire at the end of this final exercise period.

Employees of the Group who enter into a share option agreement with Festi will therefore be allowed to buy shares in the company for up to ISK 500,000 per year (the "maximum purchase price") in each exercise period, or for a total of ISK 1,000,000 during the entire two-year share option period. The number of shares covered by the share option in each period is determined by the maximum purchase price and the option price stated in the share option agreement.

11. Am I allowed to exercise the share option in part or defer the exercise of the share option between periods?

Yes, you are allowed to exercise the share option in part (for instance, by purchasing shares for ISK 250,000 or some other amount of your choice up to the maximum amount per exercise period) as well as to defer exercising the share option entirely from one exercise period to another. You are thus allowed to defer your exercise of the share option, in whole or in part, during the first exercise period until the second exercise period.

Efter the final excercise period all unexercised options will expire.

12. Will my unexercised share option automatically be carried over to the next exercise period?

Yes, your unexcercised share options from the first period transfer automatically to the second.

At the end of the second period, all unexercised options will expire.

13. How do I notify if I want to exercise the stock option?

Instructions will be sent in April 2026 to those who have signed the agreement before end of day 6 May 2025.

14. What happens if I exercise the stock option?

If you exercise the share option, you will acquire shares in Festi in return for paying the purchase price and will thereby become a shareholder in the company. Shares purchased under a share option agreement come with all the same rights as other shares in the company

If you exercise your share option, in whole or in part, you must pay for the shares in cash according to the price stipulated in the share option agreement.

In order to receive the shares, you must have a securities custody account. You can open a custody account with your current bank or with another bank in Iceland. Further details about this arrangement will be sent in April 2026 to those who sign the share option agreement by the end of day on Tuesday, 6 May 2025.

15. If I exercise my option, can I sell the shares immediately?

Yes, if you exercise a share option and receive shares in return for the agreed payment, it is entirely up to you what to do with the shares you have purchased. For instance, you can choose to hold some or all of the shares and thus remain a shareholder in the company or sell them in whole or in part.

16. Can I lose money from exercising the share option?

Buying shares involves risk. If the share option is exercised, a loss may result from the transaction if the market price of the shares falls below the purchase price after the option has been exercised.

17. If I sign the agreement, do I have to excercise the option?

No, it is always up to you to decide within each exercise period whether and to what extent you wish to exercise the share option. It is important to keep in mind that the share option is a right and not an obligation. Therefore, entering into a share option agreement does not impose an obligation on you to exercise the share option during any of the exercise periods.

However, an unexercised share option will expire at the end of the final exercise period.

18. How are stock option gains taxed?

The general rule is that the difference between the market price and the sale price/purchase price will be considered a wage payment that is subject to the same tax treatment as other wage payments.

Employees who exercise the option to buy shares, without selling them again in the same year, are to record their shares as assets in their tax return. The profit from such a transaction, i.e. the difference between the market price and the price that the employee paid for the shares, is not taxed immediately, but rather when the shares change hands (when the employee sells the shares).

If certain conditions are met, such a profit from shares may be treated as capital gains earned by the employee at the time when the shares are sold - and thus be taxed at a lower tax rate than wage income. For the profit from the purchase of shares under a share option agreement to be taxed as capital gains, employees must hold the shares for two years after the exercise of the share option. If this is not done, the profit will be taxed according to the general rule of treating it as wage income.

Employees themselves are responsible for any taxes that may be imposed due to the exercise of the share option. Festi is not responsible for the tax consequences resulting from an employee’s exercise of a share option or disposition of purchased shares.

19. Am I allowed to assign the share option or pledge it?

No, you are not allowed to assign or pledge the share option.

20. Will the share option expire if I stop working for the Group?

The share option will vest proportionally for each month that you are a permanent employee during the vesting period.

The vesting of a share option is subject to the condition that you are employed by the Group. If you stop working for the Group before the end of the two-year share option period, you will not acquire any further share options, and vested but unexercised share options will generally expire.

However, a vested share option will not expire if you are dismissed from your job without the dismissal being attributable to non-fulfilment of the employment contract or other job duties, or if your departure from Group is the result of age, death or incapacity due to ill health.

21. Can I sell the shares immediately after buying them?

There are no restrictions attached to the purchase of the shares, so after you have paid for the shares, you will receive the shares from Festi into your custody account at your bank. You are then free to sell the shares on Nasdaq Iceland at any time.

The sales profit from the transaction, i.e. the difference between the purchase price and the sale price of the shares, is taxed as income unless you hold the shares for more than 2 years, in which case the sales profit will be taxed as capital gains.

Example 1:

Year 1: A share option is exercised to purchase shares for ISK 500 thousand, but their market value on that day on Nasdaq Iceland is ISK 600 thousand. The employee decides to sell the shares immediately, generating a sales profit of ISK 100 thousand. The employee is required to pay income tax (currently 37.99% for income that falls in tax bracket 2) on the sales profit, so that the total tax payable is ISK 37,990. Thus, the employee’s net profit from the share option agreement is 100,000 – 37,980 = ISK 62,010.

Example 2:

Year 1: A share option is exercised to purchase shares for ISK 500 thousand, but their market value on that day on Nasdaq Iceland is ISK 600 thousand. The employee decides to wait to sell the shares and holds them for two years. At that time the market value of the shares is ISK 700 thousand, generating a sales profit of ISK 200 thousand. The employee pays capital gains tax (currently 22.00%) on the sales profit, so that the total tax payable is ISK 44,000. Thus, the employee’s net profit from the share option agreement is 200,000 – 44,000 = ISK 156,000.

Example 3:

Year 1: During the exercise period, the market price of Festi's shares on the Iceland Stock Exchange is lower than the option price according to the option agreement. For this reason, the employee decides not to exercise his option to buy. Where an employee's vested option is not exercised, the option is automatically transferred to year 2 and the employee is then authorized to exercise the option for up to ISK 1,000,000.